EUROPEAN AI IS MULTILINGUAL AND IT PROTECTS YOUR DATA

If you ask ChatGPT a question, it reasons in English and then translates its answer into your language. Same with DeepSeek: it reasons in Chinese and then translates its answer into your language.

In Europe, Mistral AI works in a different way. It reasons natively in 8 foundational languages: English, French, Spanish, German, Italian, Arabic, Russian and simplified Chinese.

Significantly, Mistral AI is much more protective of your data. Explicitly designed to uphold EU digital sovereignty, it respects European GDPR rules and the EU AI Act.

But it’s not just in the data protection area and the chatbot space that Europe is taking a different path. Europe also supplies a significant portion of the electrical kit that data centres need in order to be able to function.

MAUs

In October 2025, ChatGPT reached 800 million weekly active users, according to OpenAI CEO Sam Altman, as reported by TechCrunch.com. The site also reported that Google’s Gemini app had surpassed a monthly active user (MAU) figure of 750 million. In China, ByteDance’s AI assistant Doubao recorded 227 million monthly active users in December 2025, according to business intelligence provider QuestMobile. That figure puts Doubao well ahead of the pack in China as a general purpose AI assistant; its MAU number is equal to the combined total of numbers 2 through 5, namely DeepSeek (135.57 million), Tencent’s Yuanbao (40.71 million), and Alibaba’s Ant Afu (26.89 million) and Qwen (25.17 million).

In comparison, the mistral.ai website received 9.34 million visits in February 2026, according to tech platform Bayelsa Watch.

But Mistral AI is surging. Created in 2023 by three Frenchmen who had previously worked at Meta and Google, the company is now valued at EUR 11.7 billion, making it the most highly-valued AI company in Europe.

Mistral is a standout among hundreds of companies that are emerging in the European AI, quantum, semiconductor and space sectors. In France, the number of “tech unicorns” – i.e. start-ups valued at more than a billion dollars – has risen from four to 34 in just five years, according to Les Echos, a leading French economic daily newspaper.

Data Centres

Worldwide, there is a frenzy of data centre construction.

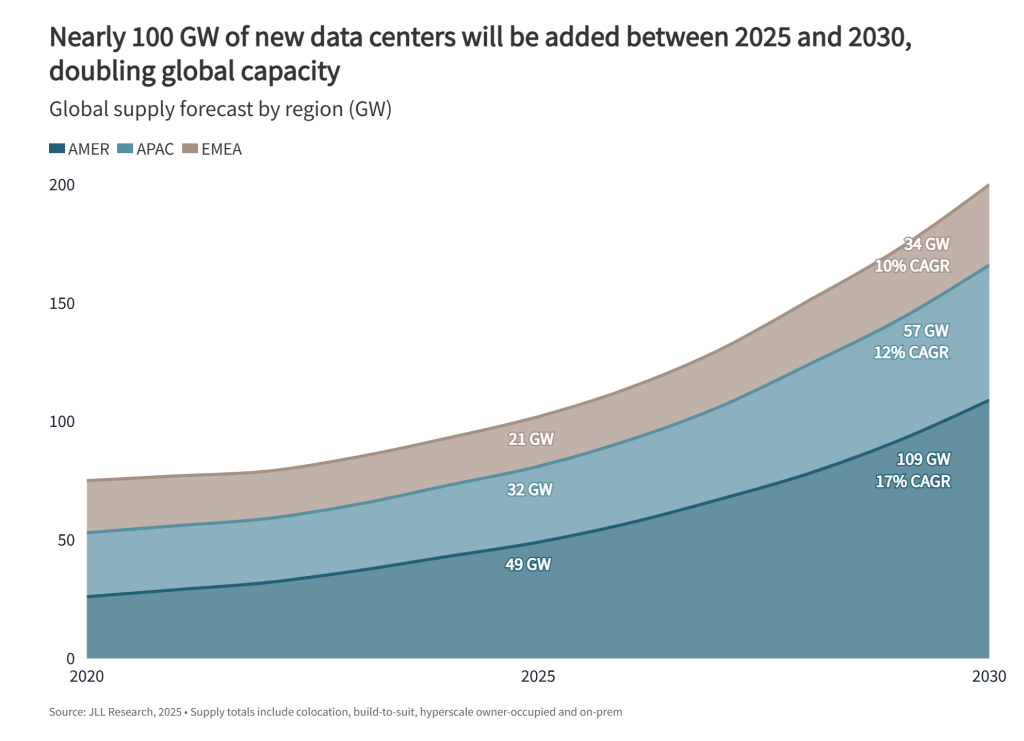

Nearly 100 GW of new data centres will be added between 2026 and 2030, doubling global capacity, according to JLL, a real estate services and investment management company. The global data centre sector will likely expand at a 14% CAGR through 2030, the firm said in its 2026 Global Data Center Outlook report.

The Americas are the largest data centre region, representing about 50% of global capacity and a 17% CAGR. The US drives most of the activity in the region, accounting for about 90% of the capacity.

APAC data centre capacity will expand from 32 GW to 57 GW by 2030, achieving a 12% CAGR.

The EMEA region will add 13 GW of new supply, with growth concentrated in established European hubs and emerging Middle Eastern markets.

Security concerns

Those American data centres – like the ones in “Data Center Alley” in Virginia – house a lot of European data. According to an article in Les Echos, almost 70% of European data is hosted outside the continent, mainly in the United States.

Europe spends around EUR 330 billion a year on cloud services; 80% of that goes to American companies and helps finance their technological advance.

But Europe’s concerns are not only economic.

In a world riven by tariffs, trade retaliation measures and distrust, the place where your data is housed is a matter of strategic concern. People who use Gmail or Microsoft 365 are potentially exposing their data to the US government because, even if the data is stored on servers in Europe, the US Cloud Act (2018) allows US authorities to access the data of entities linked to the United States, wherever they may be.

In 2026, Europe will ramp up its response to this challenge by launching the Estia Alliance (European Sovereign Tech Industry Alliance)i with the goal of reducing dependence on non-EU providers. The Estia Alliance aims to triple the capacity of Europe’s data centres and deploy “AI gigafactories” across the continent.

Picks and shovels

There is another, more prosaic, way in which Europe is impacting the AI revolution: electrical kit.

The American writer Mark Twain – after trying his hand unsuccessfully at mining in the 1860s – noted ruefully that “the best way to make money during a gold rush is to sell picks and shovels”.

In AI, those picks and shovels are the electrical products that allow data centres to optimise their load capacity: high-voltage cables, circuit breakers, high-density connectors, high-density cooling solutions, switchgear, transformers, server cabinets and so on.

In China, Chinese companies provide this kind of product. In the US, one major supplier is Pennsylvania-based Wesco, which posted sales in 2025 of around USD 23 billion.

But an even bigger player in the US market is a French company called Sonepar, which has been the world’s No.1 electrical equipment distribution company for over 15 years. In 2025, it racked up close to EUR 34 billion in sales.

Says CEO Philippe Delpech: “We are 60% bigger than Wesco, the world number 2″.

“Data centres are a huge growth area,” he adds. “We reckon on doubling our turnover in the United States in the next few years to reach a market share of around 16-17%, the same as we have in Europe”.

Other European companies, like Siemens, Schneider Electric, ABB and AEG Power Solutions, are also muscling in.

Whether it be at the macro level, in terms of the models and chat interfaces used or the centres in which data is housed, or at the granular level, in terms of the uninterrupted power supply (UPS) systems that allow data centres to function, Europeans are making their presence felt.